Last Updated on May 11, 2026

If you’ve ever applied for a personal loan, home loan, or credit card, you may have come across the term FOIR. so What Is the Meaning of FOIR? Banks and financial institutions use it to decide whether you qualify for a loan and how much they can safely lend you.

But what exactly does FOIR mean, and why is it so important in personal finance? 🤔

In simple terms, FOIR helps lenders understand how much of your monthly income is already committed to existing debts and expenses. A lower FOIR usually means better loan eligibility, while a higher FOIR may reduce your chances of approval.

This guide explains everything you need to know about FOIR, including its meaning, calculation, importance, examples, ideal percentage, comparison with similar financial ratios, and FAQs.

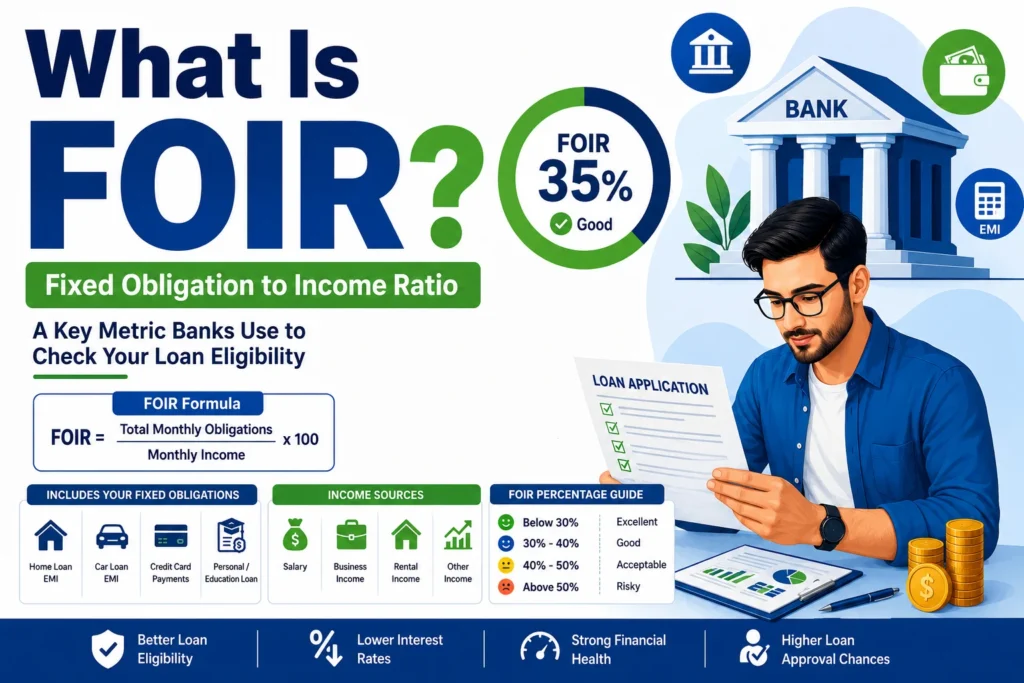

What Is the Meaning of FOIR?

FOIR stands for Fixed Obligation to Income Ratio. It is a financial metric used by banks and lenders to measure how much of a person’s monthly income goes toward fixed financial obligations such as EMIs, loans, rent, and credit card payments.

The formula for FOIR is:FOIR=Monthly IncomeTotal Monthly Obligations×100

A lower FOIR indicates better repayment capacity, while a higher FOIR suggests financial stress and lower loan eligibility.

Understanding FOIR in Simple Words

Imagine you earn $3,000 per month. Out of that:

- $500 goes to a car loan EMI

- $300 goes to a personal loan

- $200 goes to credit card bills

Your total monthly obligations are $1,000.

So your FOIR would be:30001000×100=33.3%

This means around one-third of your income is already committed to debt payments.

Banks use this number to decide whether you can comfortably handle another loan.

Full Form of FOIR

| Abbreviation | Full Form |

|---|---|

| FOIR | Fixed Obligation to Income Ratio |

Sometimes it may also be called:

- Fixed Obligations Income Ratio

- Financial Obligation Ratio

- Debt-to-Income style metric

However, “Fixed Obligation to Income Ratio” is the most commonly accepted meaning in banking and finance.

Why Is FOIR Important?

FOIR is one of the most important factors lenders consider before approving loans.

It helps banks answer questions like:

- Can the borrower repay the loan comfortably?

- Does the borrower already have too much debt?

- Is lending to this person risky?

A healthy FOIR shows financial discipline and repayment ability.

Why Banks Care About FOIR

Banks want to reduce the risk of loan defaults. If too much of your income is already tied up in obligations, there’s a higher chance you may struggle with new EMIs.

That’s why lenders prefer borrowers with lower FOIR percentages.

How FOIR Is Calculated

The calculation is straightforward.

FOIR Formula

FOIR=Gross Monthly IncomeTotal Fixed Monthly Obligations×100

What Counts as Fixed Obligations?

Fixed obligations may include:

- Existing loan EMIs

- Credit card dues

- Car loan payments

- Home loan EMIs

- Student loan repayments

- Rent obligations (sometimes)

- Other recurring financial commitments

What Counts as Income?

Income generally includes:

- Monthly salary

- Business income

- Rental income

- Pension income

- Freelance income (if accepted by lender)

FOIR Calculation Example Table

Example 1: Salaried Employee

| Details | Amount |

|---|---|

| Monthly Salary | $4,000 |

| Car Loan EMI | $400 |

| Personal Loan EMI | $300 |

| Credit Card Payments | $200 |

| Total Obligations | $900 |

| FOIR | 22.5% |

Calculation:4000900×100=22.5%

This is considered a healthy FOIR.

Example 2: High Debt Situation

| Details | Amount |

|---|---|

| Monthly Income | $2,500 |

| Existing EMIs | $1,500 |

| FOIR | 60% |

A 60% FOIR is relatively high and may reduce loan approval chances.

Ideal FOIR Percentage

Different lenders have different acceptable FOIR limits.

However, here’s a general guideline:

| FOIR Percentage | Meaning |

|---|---|

| Below 30% | Excellent |

| 30%–40% | Good |

| 40%–50% | Acceptable |

| Above 50% | Risky |

| Above 60% | High rejection possibility |

Most banks prefer FOIR between 40% and 50%.

How FOIR Affects Loan Approval

FOIR directly impacts:

- Loan eligibility

- Loan amount

- Interest rate

- Approval speed

- Creditworthiness

Lower FOIR = Better Chances ✅

A lower FOIR suggests:

- Better money management

- Lower financial stress

- Strong repayment capacity

This often results in:

- Easier approvals

- Higher loan amounts

- Better interest rates

Higher FOIR = Riskier Borrower ⚠️

A high FOIR can signal:

- Too much existing debt

- Reduced repayment ability

- Higher default risk

Banks may:

- Reject the loan

- Reduce loan amount

- Ask for collateral

- Charge higher interest

FOIR vs Debt-to-Income Ratio (DTI)

People often confuse FOIR with DTI because both measure debt burden.

Here’s the difference:

| Feature | FOIR | DTI |

|---|---|---|

| Full Form | Fixed Obligation to Income Ratio | Debt-to-Income Ratio |

| Common Usage | India & Asian banking systems | US & international lending |

| Includes Fixed Obligations | Yes | Yes |

| Used For | Loan eligibility | Mortgage and debt assessment |

| Purpose | Assess repayment capacity | Evaluate debt burden |

Both concepts are similar, but FOIR is more commonly used in Indian banking terminology.

FOIR in Different Types of Loans

Home Loans

For home loans, lenders pay close attention to FOIR because these loans involve large amounts and long repayment periods.

Typical acceptable FOIR:

- Up to 50%

Personal Loans

Since personal loans are unsecured, lenders prefer lower FOIR.

Typical acceptable FOIR:

- 40%–45%

Car Loans

Car loans may allow slightly higher FOIR if income is stable.

Credit Cards

Banks also assess FOIR before approving high-limit credit cards.

Factors That Influence FOIR

Several things can impact your FOIR score.

Existing Loans

More loans increase obligations and raise FOIR.

Income Level

Higher income generally lowers FOIR percentage.

Credit Card Usage

Large recurring card payments can increase FOIR.

Loan Tenure

Longer tenure may reduce monthly EMI and improve FOIR.

Lifestyle Expenses

Some lenders also consider recurring commitments and living costs.

How to Improve Your FOIR

Improving your FOIR can significantly increase loan approval chances.

1. Pay Off Existing Debt

Reducing outstanding loans lowers monthly obligations.

2. Avoid Multiple Loans

Too many EMIs increase FOIR quickly.

3. Increase Income

Salary hikes, side income, or business growth improve the ratio.

4. Extend Loan Tenure

Longer repayment periods reduce monthly EMI amounts.

5. Limit Credit Card Debt

Keep card balances manageable.

Real-World Example of FOIR

Let’s say Rahul earns ₹80,000 per month.

His monthly obligations:

- Home loan EMI: ₹20,000

- Car loan EMI: ₹10,000

- Credit card dues: ₹5,000

Total obligations:

₹35,000

FOIR calculation:8000035000×100=43.75%

This FOIR is generally acceptable for many lenders.

If Rahul applies for another large loan, the bank may still approve it, but only after checking whether the new EMI keeps FOIR within acceptable limits.

Origin and Popularity of FOIR

FOIR became popular as banks developed more structured risk assessment systems.

Financial institutions needed a quick way to evaluate:

- Borrower repayment ability

- Financial discipline

- Debt exposure

Today, FOIR is widely used in:

- Retail banking

- Mortgage lending

- Credit card approvals

- Consumer finance

- Business lending

It is especially common in countries with formalized credit evaluation systems.

Common Misunderstandings About FOIR

“FOIR Is the Same as Credit Score”

Not true.

- Credit score measures credit history and repayment behavior.

- FOIR measures current debt burden versus income.

Both are important, but they are different metrics.

“High Salary Means Automatic Approval”

Even high earners can get rejected if their FOIR is too high.

“FOIR Only Matters for Big Loans”

Even small personal loans may involve FOIR checks.

Alternate Meanings of FOIR

Although FOIR is mostly associated with finance and banking, the abbreviation may occasionally have alternate meanings in niche industries.

However, in common usage, especially online and in banking, FOIR almost always refers to:

Fixed Obligation to Income Ratio

Professional and Financial Alternatives to FOIR

Some lenders or financial systems may use related terms such as:

| Term | Meaning |

|---|---|

| DTI Ratio | Debt-to-Income Ratio |

| Debt Burden Ratio | Measures debt obligations |

| Income Obligation Ratio | Similar concept |

| Credit Utilization Assessment | Credit burden analysis |

FOIR Usage Examples

Friendly Financial Advice

“Try reducing your existing EMIs before applying for a new loan so your FOIR improves 😊”

Neutral Banking Statement

“The applicant’s FOIR exceeds the acceptable threshold.”

Negative or Dismissive Tone

“Your FOIR is too high for loan approval at the moment.”

Key Benefits of Maintaining a Healthy FOIR

Keeping FOIR low offers several benefits:

- Better loan eligibility

- Higher approval chances

- Lower financial stress

- Improved financial planning

- Better creditworthiness

- Easier future borrowing

Quick FOIR Checklist

Before applying for a loan, ask yourself:

✅ Are my existing EMIs manageable?

✅ Is my FOIR below 50%?

✅ Can I reduce unnecessary debt?

✅ Do I have stable monthly income?

✅ Am I overusing credit cards?

If most answers are yes, your loan application may have stronger approval chances.

FAQ About FOIR

1. What is the full form of FOIR?

FOIR stands for Fixed Obligation to Income Ratio.

2. What is a good FOIR for loan approval?

Generally, a FOIR below 40%–50% is considered healthy by most lenders.

3. How is FOIR calculated?

FOIR is calculated by dividing total monthly obligations by monthly income and multiplying by 100.

4. Does FOIR affect credit score?

Not directly. FOIR and credit score are separate financial metrics.

5. Can a loan be rejected because of high FOIR?

Yes. A very high FOIR may indicate repayment risk and lead to rejection.

6. What expenses are included in FOIR?

Typical expenses include:

- Loan EMIs

- Credit card payments

- Recurring debt obligations

- Sometimes rent payments

7. Is FOIR important for home loans?

Yes. Banks heavily evaluate FOIR before approving home loans.

8. How can I reduce my FOIR quickly?

You can:

- Pay off loans

- Reduce credit card debt

- Increase income

- Consolidate debts

- Extend loan tenure

Conclusion

FOIR is one of the most important financial ratios used by banks and lenders to evaluate borrowing capacity. It helps determine whether a person can comfortably manage existing obligations along with new loan repayments.

In simple terms:

- Lower FOIR = healthier finances ✅

- Higher FOIR = greater financial stress ⚠️

Understanding your FOIR can help you:

- Improve loan eligibility

- Make smarter financial decisions

- Reduce debt burden

- Maintain long-term financial stability

Before applying for any loan, it’s a smart idea to calculate your FOIR and improve it if necessary. Even small financial adjustments can make a big difference in approval chances and interest rates

James Colton is a language researcher and content writer who loves exploring the deeper meanings behind everyday words. With a background in linguistics, he breaks down complex terms into simple, clear explanations that anyone can understand.